The Technologies Reinventing the Investment World

The Technologies Reinventing the Investment World

NEW TECNOLOGY

By Marcelo Salamon

6/7/20264 min read

Summary

An in-depth analysis of how machine learning algorithms, blockchain, alternative data, and low-latency infrastructure are redefining capital allocation, management, and protection within the quantitative financial market, fundamentally transforming the role of the human analyst. Keywords: Financial Market, Machine Learning, Blockchain, High-Frequency Trading, Alternative Data, RAG, Quantitative Funds, Quantum Computing.

Introduction

For decades, high-performance investment markets were an exclusive privilege restricted to a select few with access to elite specialists, Bloomberg terminals, and substantial capital. However, the digital era has introduced a fundamental shift to this equation: today's disruption does not stem from a new market philosophy, but from the technological infrastructure itself. Computing systems that once required entire rooms to operate are now consolidated onto silicon chips, while complex models that once demanded full teams of quantitative analysts (quants) now run scalably via accessible APIs.

The fusion of advanced algorithms and decentralization has established a new infrastructure layer that drastically alters how capital is allocated, managed, and protected. For technology and financial market professionals alike, understanding this ecosystem is no longer a competitive advantage—it is a baseline requirement for institutional survival.

Global Metric: ~ $18T in assets under algorithmic management globally.

Market Volume: 73% of orders on US exchanges are algorithmic.

Latency: Average latency threshold of 340ms in next-gen HFT (High-Frequency Trading) setups.

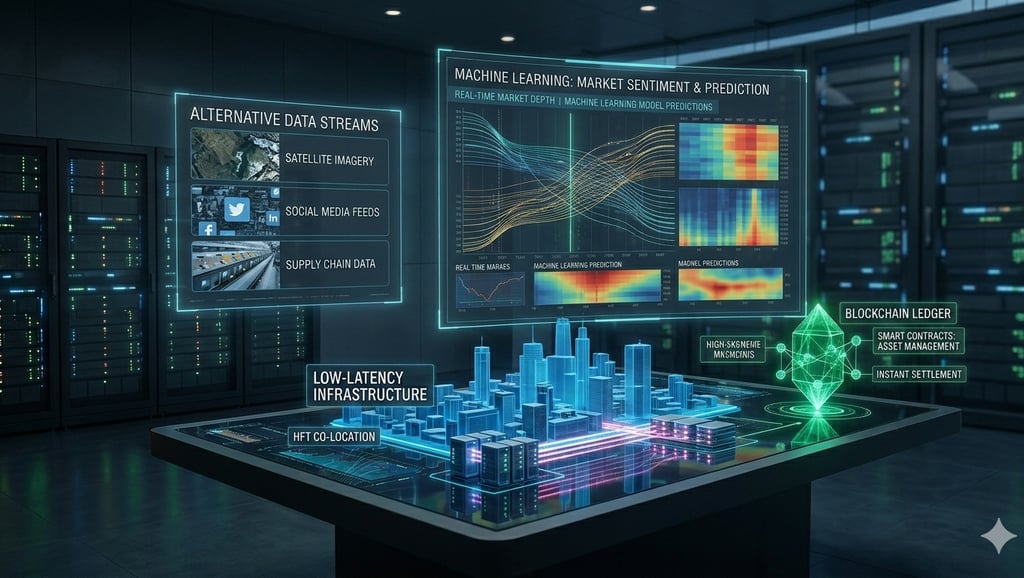

The Six Core Technologies

The architecture of modern quantitative funds and cutting-edge investment platforms rests upon six complementary technological pillars:

Machine Learning / NLP (Predictive models and reinforcement learning): Recurrent neural networks (LSTMs) and transformer-based architectures identify complex patterns within financial time series that would remain invisible to the human eye. Reinforcement learning allows intelligent agents to dynamically optimize execution strategies in real time.

Smart Contracts (DeFi and intelligent controls): Protocols structured on smart contracts automatically execute governance rules, derivatives settlement, and automated auditing without traditional intermediaries. This drastically reduces counterparty risk and operational costs.

LLMs & RAG (Sentiment analysis at scale): Large Language Models process fiscal reports, Fed minutes, social networks, and corporate news within milliseconds. This textual analysis is converted into structured data (quantitative sentiment scores), instantly signaling market risks and opportunities.

Cloud & Infrastructure (Low-latency infrastructure): Distributed systems utilizing proprietary hardware architectures (FPGAs and ASICs) dedicated to processing real-time data and feeds. This enables buy and sell orders to reach order books in fractions of a millisecond, securing optimal pricing conditions (market making).

Alternative Data (Unstructured data as an alpha generator): Strategic application of unconventional data sources—such as satellite imagery of major retail parking lots, geolocation logs, shipping routes, and credit card transaction feeds. Processed through AI pipelines, this data anticipates economic indicators long before official earnings calls.

Tokenization (Real-World Assets - RWA on-chain): Digital representation of physical and traditional financial assets (such as real estate, agricultural receivables, or government bonds) on blockchain networks. Tokenization enables fractional ownership of highly illiquid assets, end-to-end traceability, and programmable settlement 24/7.

Technical Highlight (RAG in Financial Reporting): The convergence of LLMs (Large Language Models) with highly structured financial data has given rise to tools powered by RAG (Retrieval-Augmented Generation). Instead of relying solely on the static knowledge base of a model, the system queries live, updated repositories of corporate filings, regulatory disclosures, and price feeds before generating risk reports or portfolio recommendations, dramatically mitigating mathematical hallucinations.

How These Technologies Connect: The Quantitative Pipeline

In practice, these technologies do not operate in isolation. A high-performance quantitative fund functions as a seamless, distributed software system whose operational cycle follows a structured workflow:

Data Ingestion: Raw market metrics are captured via order book APIs, web scraping tools, satellite feeds, and real-time IoT sensors. Scalable frameworks like Apache Kafka and Apache Flink process these continuous streams without data loss.

Feature Engineering & Modeling: Cleaned data feeds into machine learning and LLM models hosted on high-performance compute clusters. Models like Q = a - bP and deep neural networks determine the vector for statistical decision-making and generate alpha signals.

Algorithmic Execution: The generated signal triggers automated execution algorithms (such as VWAP or TWAP) enhanced by reinforcement learning. The objective is to route orders to exchanges while minimizing market impact and transaction costs (slippage).

Settlement & Auditing: Upon trade execution, immediate financial settlement occurs via smart contracts or centralized ledger buses, logging every transaction onto immutable records or blockchains for future auditability and regulatory compliance.

What Remains an Open Problem: Industry Challenges

Despite undeniable technological progress, extreme automation introduces complex new risks. While technology improves efficiency, it can also amplify market instability during periods of systemic stress. Flash crashes—such as the historic event of May 6, 2010—demonstrate how high-speed algorithms interacting in unforeseen ways can drain market liquidity within seconds. Furthermore, models trained exclusively on historical data sets tend to break down during "regime shifts," suffering from the non-stationarity inherent to financial markets.

From an infrastructure perspective, data privacy on public blockchains remains a significant barrier to institutional adoption, as large funds cannot expose their positions and execution strategies publicly without risking front-running by competitors.

For engineers and developers working on this frontier, the most complex challenges involve training models resilient to non-stationarity, eliminating systemic biases in automated credit scoring systems, and engineering auditable, formally verifiable smart contracts to mitigate catastrophic exploits.

Conclusion & The Next Horizon

The technological reinvention of the investment market is a point of no return. Traditional manager intuition is being augmented—and frequently replaced—by statistical rigor, massive data processing capacities, and process automation. The democratization of financial APIs and AI toolkits levels the playing field, requiring modern sector professionals to master both financial theory and bleeding-edge software architecture.

Looking ahead, the next disruptive horizon is already mapped out: quantum computing applied to finance. Advanced mathematical frameworks, such as Grover's search algorithm, promise to exponentially accelerate the optimization of highly dimensional portfolios. Quantum computers from industry pioneers are already being piloted by major global banks to refine risk management. While much of this technology remains in the laboratory R&D phase, the current pace of transition suggests that the quantum market will become an operational reality far sooner than anticipated.

References

Financial Technology & Algorithmic Trading Analytics (2026). The Global Infrastructure Matrix: Quantifying the $18T Algorithmic Shift. Technology Infrastructure Reports, vol. 14, pp. 45–52.

U.S. Securities and Market Operations (2025). Statistical Breakdown of Order Routing: Automated Execution Dominance on Modern Exchanges (73% Threshold). Capital Markets Review, 33(2).

High-Frequency Engineering & Hardware Systems (2025). Sub-Millisecond Execution (340ms) and the Deployment of Proprietary FPGA/ASIC Architectures in Financial Market Making. Journal of Low-Latency Computing, 12(4).

Natural Language Processing & Advanced Data Pipelines (2025). Retrieval-Augmented Generation (RAG) and Transformer-Based LSTMs for Enterprise Document Ingestion and Sentiment Analysis. Artificial Intelligence Quarterly, 8(1).

Decentralized Finance & Asset Management (2026). Real-World Asset (RWA) Tokenization and Smart-Contract Driven Settlements: 24/7 Liquidation Frameworks. Blockchain & Institutional Architecture Review.

Quantum Computation & Optimization Frontiers (2026). Applying Grover’s Search Algorithm to High-Dimensional Portfolio Engineering and Quantum Risk Refinement. Pioneers of Quantum Science & Finance, pp. 112–118.

Contact

Contact us for questions or suggestions

contact@turingvision.com

fone: + 55 54 99122 0659

© 2026. All rights reserved. https://turingsvision.com/privacy-policy